After the financial crisis of 2008 through 2017, the Central Park market was one of the most resilient in the city, even exceeding Park and Fifth Avenues. Thereafter, in the years leading up to the pandemic, there were shifts in the desirability of prewar apartments in general, and we began to see the effects of those changes in apartments sitting longer on the market. Part of the reason for the change was the advent of brand-new buildings on the Upper West Side which have many amenities and were free of the co-op board process. After the pandemic, many prewar apartments that needed work sat on the market as costs to renovate nearly doubled with higher labor costs and supply chain challenges. New Developments became even more appealing to buyers. In fact, to this day, an apartment that needs work or has a flaw in the layout or views has more impact on price now than in the recent past. Large Central Park West co-op sales improved a bit since the early post-pandemic days. Buyers have been gravitating back to these grand and gracious homes as they provide proximity to the Park, schools, and have the appeal of historically prestigious white glove buildings. In addition, buyers value the gorgeous year-round seasonal views of Central Park. While high-interest rates and uncertainty drove sales down last year, the number of contracts of large co-op sales on Central Park West far outnumbered larger co-op sales on the rest of the Upper West Side; over 70% of $4M+ co-op contracts were either on CPW or just off it.

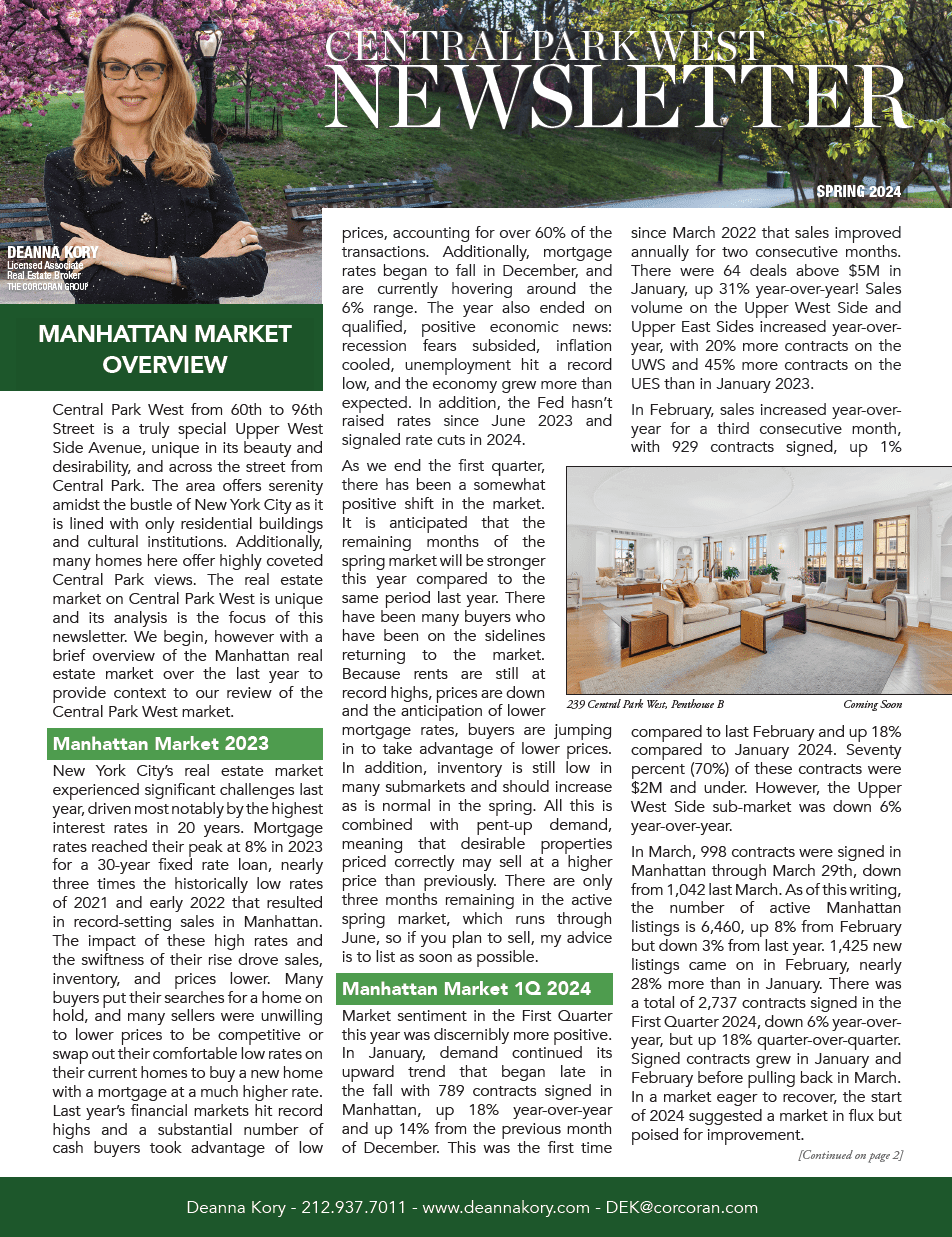

In this newsletter we provide an overview of the Manhattan Market, a Central Park West Market snapshot, an analysis of the luxury market on Central Park West, and advice for sellers on what to expect this spring.

Click here to download the report.